Equities

US Stocks

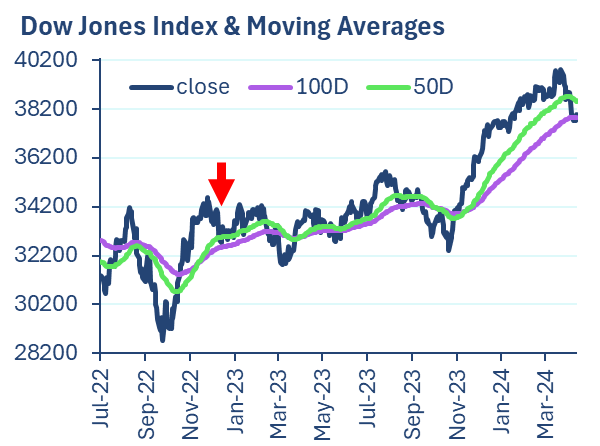

As of April 19th, 2024, the Dow Jones has been in drawdown for 3 weeks, finishing 4.6 percent off its last All Time High of 39,807. Active traders are taking money off the table as the major US indices – the Dow, S&P, and NASDAQ – break below key moving averages. The Dow is now trading below the 50-day and, so far, is finding support above the 100-day. If it closes below the 100-day, we’re likely to see another pullback as more traders exit positions.

Exits from stock-related funds were the largest since mid-December 2022 (marked with a red arrow on the chart). As always, the media has to find a cause for every bump in the road. This week, the reasons were higher future interest rates and war in the Middle East. Those were probably drivers for some investors, but I invite anyone who thinks there has to be a reason behind every selloff to consult Matthew McConaughey from Wolf of Wall Street (1:47).

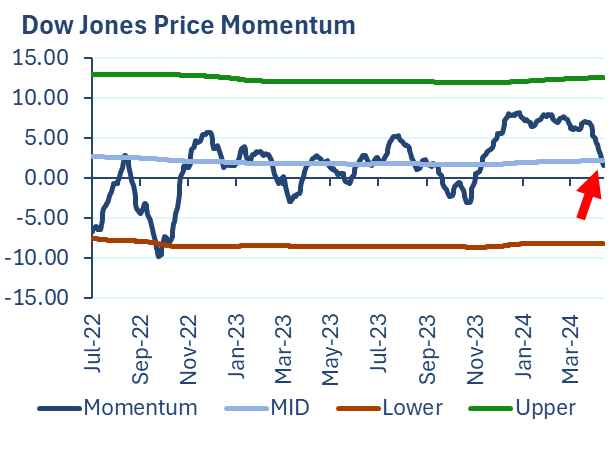

Price momentum took a dive from the first week of April onward, and finally crossed below the midpoint of my preferred range last week. Momentum traders will likely help push stock prices down as they follow this signal into short trades.

Investors who bought US stock funds 3 months ago saw all gains eaten away by last week’s selloff. Those who got in 6 and 12 months ago are still in the green.

Rolling US Equity Returns (Dow Jones Index)

| As of Date | 3 month | 6 month | 12 month |

| 4/19/2024 | -0.16 | 17.18 | 13.37 |

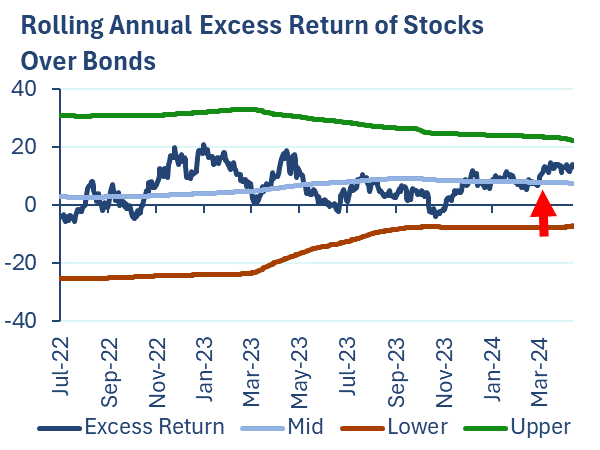

Most financial assets are prone to sell off with an increased probability of higher future interest rates. We would expect bonds to hurt more than stocks, and that’s what we’ve seen. Bonds have been performing “extra” badly, compared to stocks, since February.

A couple of takeaways from this. First: “high rates” really does mean high rates. The longer they stay high the less likely is a recovery in the price of the paper held in these large bond index funds. Second: the Middle East situation is heating up, but not yet enough to turn financial markets from “risk on” to “risk off”. In other words, the moment when investors are frightened enough that they dump stocks in favor of the ole’ reliable US Treasury has not yet arrived.

Adjusting for Inflation

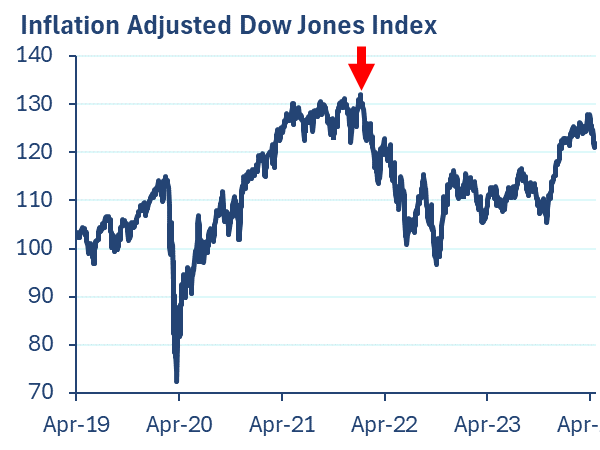

The major US Indices haven’t reached a new high since December 2021.

That doesn’t mean investors shouldn’t have any exposure to US stocks, we’re just adjusting for the reality that dollars buy less than they used to. As of April 19th, the Dow is 7.6 percent below its all time high.

“Rest of the World” Equities

The US equity allocation of your 401(k) continues to outperform the global equity allocation, as it has for several years. Here we use the Vanguard Global Equity Ex-US fund as a proxy (VXUS). Returns correlated quite well coming out of the 2022 bear market, then diverged in October 2023. At the time, I was writing about the worsening real estate crisis in China. This is also when the IDF ramped up its attacks on the Gaza strip in response to October 7th. The fourth quarter of 2023 is also when the UK and Japan (large components of the VXUS fund) entered recession.

US vs “Global Ex-US” Equities – Percent change in 2 years

Dow Jones Industrial Average: 22.09

VXUS (Vanguard Global Equity Ex-US ETF): 14.86

Bonds & Rates

I recently heard a respected podcaster in the finance community claim that “10-year treasury yields have barely budged in three years”. Not so, in fact, quite the opposite. The 10-year Treasury yield (as well as most other yields longer than 2 years) have followed a textbook upward trend since 2021.

This is still a problem – and will continue to be a problem – for bonds and the institutions that own them.

The average interest rate on the bonds in most of the major funds is 2 ½ percent. The average bond in the S&P US Treasury index doesn’t mature for another 6 years and trades at a price of 91 cents on the dollar. Most US bond funds are tracking that index or others like it. That means (very roughly) that if rates remain at current levels, it will be another 3 years before the average bond trades for 100 cents on the dollar or more. With the rapid rise in rates has, as we should expect, come a drop in the value of bond funds. Surprisingly enough, the junk bond fund HYG has performed the “least bad” out of the largest funds.

3-Year Return in Large US Bond Funds

TLT (20-year+ US Treasuries): -26.24, MBB (Mortgage Backed): -8.16,

LQD (Investment Grade Corporate): -7.41, HYG (High Yield “Junk” Corporate): -4.14

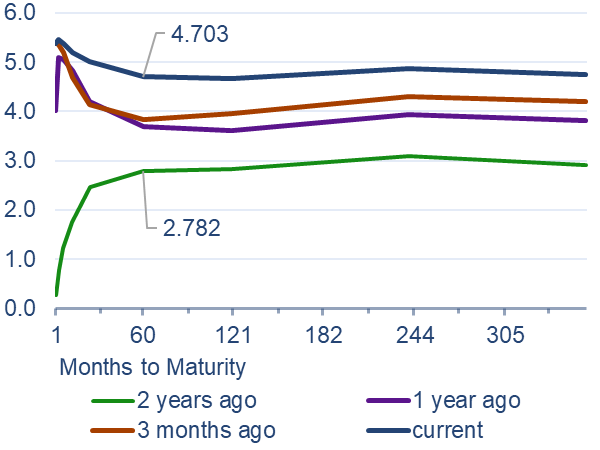

Treasury yields for terms of 5 years or more have shifted up by about a full percentage point over the last year (the 10-year, for example, shifted from 3.6 to 4.7).

US Treasury Yield Curve

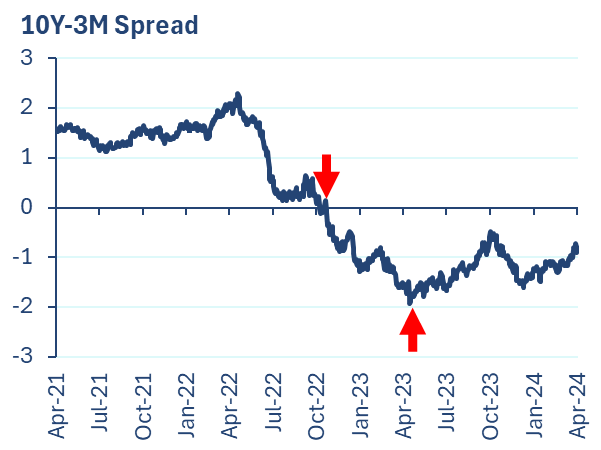

The spread between 10-year and 3-month treasuries is still quite negative, giving off the infamous “inverted yield curve” signal that many intelligent people are ready to declare is dead. The curve has now been inverted – meaning rates are out of the norm because 10-year gov’t bonds are paying lower rates than 3-month gov’t bonds – for 18 months. It has inched closer to “un” inversion since June 2023, driven by the 10-year bond yield rising.

Rate Futures

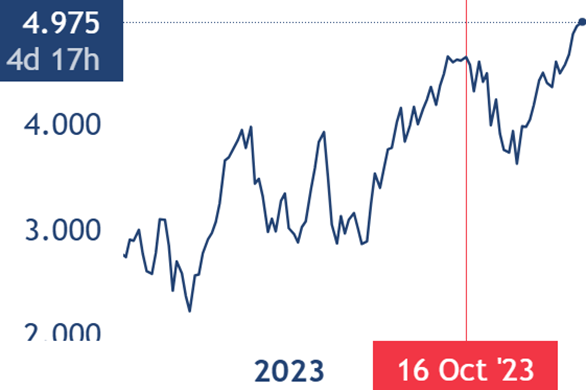

We mark October 2023 as roughly the moment that the central banks began to “talk” interest rate expectations down, using speeches and favored journalists to whisper their confidence that inflation had been beat.

Markets listened and began pricing in aggressive cuts. But over the last quarter, the interest rate on the December 2024 Futures contract (and all others) has risen. We started the year with the market pricing in seven rate cuts by December, now we’re down to one.

Commodities – Oil and Gold Continue to Surge

The commodity indices have yet to make new highs since their massive bull markets in Spring 2022 but have surged since late December 2023. The big drivers are energies and metals; most of the major “soft” (agricultural) commodities are down.

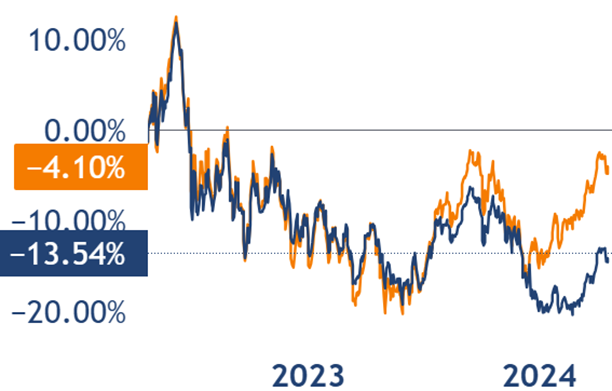

Commodity Index Tracking ETFs since April 2022

GSG (Goldman Sachs Commodity Index Tracking Fund): -4.1

DBC (Deutsche Bank Commodity Index Tracking Fund): -13.54

Key Commodities and their 12-Month price changes

| Commodity | 12- month percent change |

| WTI Crude Oil | 4.50 |

| Gold | 19.1 |

| Silver | 10.5 |

| Copper | 14 |

| Wheat | -13.5 |

| Corn | -33.6 |

| Soy | -19.1 |

Buy the pre-halving, sell the post-halving

The Bitcoin market reminded everyone why it’s a bad idea to trade the news (at least concurrently). For several weeks, now, the big story in BTC has been the “halving”. The fees for mining bitcoin are designed to shrink over time so as to reduce the speed at which new coins are minted. I’d be lying if I said I knew how many halvings there have been so far, but we had another one on April 20th – interesting choice of date. There will be another in 2028. This type of event should be bullish for the price of bitcoin because it will restrict further supply. Low supply plus same demand equals higher price.

BTC’s price broke out in October (another reflection of easy financial conditions), advanced until the second week of march, and has pulled back about 9 percent since. It’s quite normal in financial markets for a price to advance in anticipation of an event that “should” push the price higher. When the event comes, there’s often a pull-back, or worse.

Bitcoin/USD Price with 100-day moving average

Traders who took breakout signals by October 31st are up about 130 percent as the price rose from about $27,600 to $66,200.

Large-cap Cryptocurrencies and their 12-month price changes

| Crypto Asset | 12 month percent change |

| Bitcoin/USD | 133.00 |

| Ethereum/USD | 72.7 |

| Solana/USD | 600 |

| XRP/USD | 13.4 |

| Dogecoin/USD | 101 |