The “US-Saudi petrodollar deal ends after 80 years”, reads one article from India Today. Another, from NASDAQ, claims that the “U.S.-Saudi Petrodollar Pact Ends after 50 Years”. And FX Street says “The Petrodollar is Dead and That’s a Big Deal”.

Summary:

- A slew of recent articles and Twitter posts claims that Saudi Arabia allowed the “Petrodollar Pact” to expire on June 9th, 2024. Since “the agreement was a boon for the dollar and was key in cementing the greenback as the world reserve currency”, this is bad for the value of the dollar and highly inflationary. A currency crisis is around the corner, probably.

- Not one claim in any of these articles is accurate. The “Petrodollar Pact” or “Petrodollar System” is a myth. The very idea that the pact has an expiration date didn’t come about until June 2024. The theory of the Petrodollar System goes as follows.

- After Nixon ended the Gold Standard in 1971, the Arab OPEC nations, let by Saudi Arabia, doubted the stability of the dollar so much that they began refusing it as payment for their oil exports. Some also claim that they demanded to be paid in gold. In 1974, the US brokered a deal, whereby the Saudis would exclusively take dollars for their oil, while the Americans (i) promised to keep buying Saudi oil, and (ii) assisted with the Kingdom’s economic development and militarization. This put a floor under the price of the dollar, and effectively saved the US from hyperinflation.

- The Nixon Administration did make a pact with the Saudis in April 1974. It was signed in June, and Treasury Secretary William Simon added some goodies to it that July. However, that agreement had nothing to do with what currency OPEC’s oil would be sold for. Their acceptance of dollars for oil was a given.

- What Simon brokered in July of ’74 was a very specific form of “Petrodollar Recycling”. Some of Saudi’s petrodollar revenues would be invested in US Government bonds.

- Petrodollar Recycling – where Middle Eastern oil revenues are invested in dollar-denominated stocks, bonds, and bank loans – was already happening by 1974. All Simon did was bring some of the flow to the US Treasury. The very term “Petrodollar” preceded Simon’s negotiation by 9 months.

- By 1980, Saudi’s US Government Bond holdings totaled $12.2 billion, about 1.3 percent of America’s $930 billion of debt. That proportion is now about a third of a percent.

- The narrative holds that the Petrodollar established OPEC’s preference for dollars. In reality, the whole world’s preference for dollars, even after the end of the gold standard, established the Petrodollar.

- The “Petrodollar Problem”

The most consequential aspect of the Petrodollar Pact Theory is that a political agreement created the basis on which most of the world uses dollars to settle international trade. This just isn’t so.

The OPEC nations never threatened to refuse dollars as payment for oil. The Petrodollar problem was the abrupt shift in the international Balance of Payments that resulted from high oil prices. Most countries in the world were “short oil”, which means they had to import at least some of the oil they used. Since many Western economies imported much more of their oil than America’s 25 percent, those countries were far worse off than the US. This characterized most of Western Europe, Britain and Japan, whose imports were 75-95 percent of their oil consumption.

As oil prices rose, even before the October 1973 embargo, the OPEC economies realized huge Balance of Payments surpluses at the expense of the short oil economies. In just two years, from 1970 to 1972, Saudi Arabia’s foreign exchange (FX) reserves rose by 286 percent. When a country runs a balance of payments deficit, investors and traders tend to allocate away from, or even short, that currency in the foreign exchange market. Thus, the governments of the US, Europe, and Japan, all feared a currency crisis. The October 1973 embargo exacerbated this problem.

Can a country “even out” a Balance of Payments deficit? Yes, by attracting investment. If America buys a billion dollars of oil from Saudi Arabia, but then Saudi Arabia sends a billion dollars back by purchasing stocks and bonds, the imbalance is fully corrected. This is “Petrodollar Recycling”, first introduced to the House Committee on Foreign Affairs on September 6th, 1973.

Peter G. Peterson, chairman of the now-defunct Lehman Brothers investment bank, coined the term “Petrodollar” in his testimony to congress that day. He told the legislature that they needed to find ways of attracting “$10-15 billion of investments from oil producing countries to balance the rising cost of oil imports and keep the dollar’s foreign exchange value from plummeting.”

He advised that they do this by “[making] available to Middle Eastern countries the help of experts in finance, management, technology, production, and other specialities.” Finally, he urged the US to take a more “sensitive interest” in the security aspirations of those countries. To that affect, there was a pact announced in DC and Riyadh on April 5th, 1974. It just didn’t do what everyone seems to think it did, and the Americans weren’t the first ones to negotiate weapons for Middle East investment.

The Nixon Administration made a deal whereby the US would recommit to economic cooperation and weapons supplies to the Saudis. Secretary of State Henry Kissinger made a similar deal with Egypt – not an OPEC nation – a couple of weeks later. France and Britain negotiated weapons sales to the Kingdom that January. Everyone was looking to claw some of their petrodollars back.

That agreement was signed two months later in June. In July, Treasury Secretary William Simon flew to Jedda to meet with Prince Fand Ibn Abdel Aziz and iron out the details. This is the meeting that sparked a legend of its own. According to one of Simon’s subordinates, Gerry Parsky, Simon convinced the Saudis to invest (“recycle”) some of their Petrodollars into US Government Bonds. They agreed, but on the condition of anonymity. Until a Freedom of Information Act suit brought by Bloomberg in 2016, Saudi holdings of US Treasury Bonds were lumped into a broad category of “Oil Exporting Nations” in the Treasury’s monthly reports.

Even this narrative gives the central planners far too much credit. If all you had was the information above, you might be tempted to believe that the Nixon Administration invented Petrodollar Recycling. Bloomberg largely overstated the impact of William Simon’s deal with the Saudis, claiming that it would “fund America’s widening deficits”. At the margin, maybe. But if that agreement is really what saved the US Bond Market, there shouldn’t have been a “Dollar Crisis”, complete with the US borrowing Swiss Francs and German Marks, four years later. The remedy for that problem wasn’t the sale of weapons to OPEC, it was 20 percent interest rates.

2. The Eurodollar Market – Est. 1955

A year before Nixon’s economic and military pact with the Saudis, and 7 months before the 1973 Oil Embargo, it was a well-known fact that OPEC oil revenues were flowing Into the Eurodollar Market. This is a network of international banks, which had been taking dollar deposits from all over the world and lending them to any government or corporation they saw fit. This money market was “offshore”, outside the regulatory jurisdiction of the US Federal Reserve. In March 1973, American Bankers estimated that $7.5 billion of the $80 billion Eurodollar market was funded by the Middle East. Before they had been dubbed “Petrodollars”, OPEC’s dollar surpluses were already getting recycled through the Eurodollar Market.

The offshore dollar market came into existence in 1955. When the Bank of England raised their Bank Rate, it widened the spread between Britain and America’s policy interest rates. The Midland Bank borrowed Dollars instead of Pound Sterling, converted them to pounds, and lent them on. This gave them a wider interest margin than they would’ve earned if they had borrowed in British Pounds. This is now called the global “carry trade”. An international bank borrows in a large currency, one with lots of low interest rate deposits floating around; most often the borrowing currency is the dollar. It then earns an interest spread by lending either in the same currency at a higher interest rate, or in a different currency, often at a much higher interest rate. Though it was also referred to as the “Eurocurrency market”, the lion’s share of borrowing and lending was in dollars. This had become a major source of financing across the world by the 1960s, so much so that central banks had to tailor their interest rate policies around these flows of “Hot Money”. See examples here, here, and here. Even the Soviets borrowed $100 million from this offshore money market in 1975. The iron curtain never spread to the banking system.

15 years before Peter G. Peterson coined the term “Petrodollar”, the Soviets were parking theirs in the Eurodollar Market. In 1958 the Soviet-owned, London operated Moscow Narodny Bank began lending Eurodollars, which ultimately came from the USSR’s exports of wheat and oil1. In 1969, Economist Milton Friedman published a paper on the Eurodollar Market in the Morgan Guaranty (bank) survey. It’s no coincidence that his hypothetical example involves an “Arab Oil Sheikh” taking a million dollars of oil export revenue, and parking them in a Eurodollar Bank.

By December 1973, the World Bank had already began a scheme to lend Petrodollars, which they themselves borrowed from Kuwait, to developing countries, ostensibly to help keep their economies afloat.

In April 1974, after the US/Saudi cooperation pact, and before its signing, the Times reported on seven cases of direct investment of OPEC’s “new oil money” in the US. The investments totaled about a billion dollars. The “greatest single share” of the oil money, which was projected to reach $50 billion that year alone, was still funneling into the Eurodollar and foreign exchange markets. The one asset the Saudis did need convincing to buy is US government bonds. While they owned British and German bonds, “New York sources [said] they had stayed out of US Treasury Bills”. If anything, Simon’s Petrodollar Recycling agreement only diverted capital that would’ve gone to America’s private industries, to America’s government treasury.

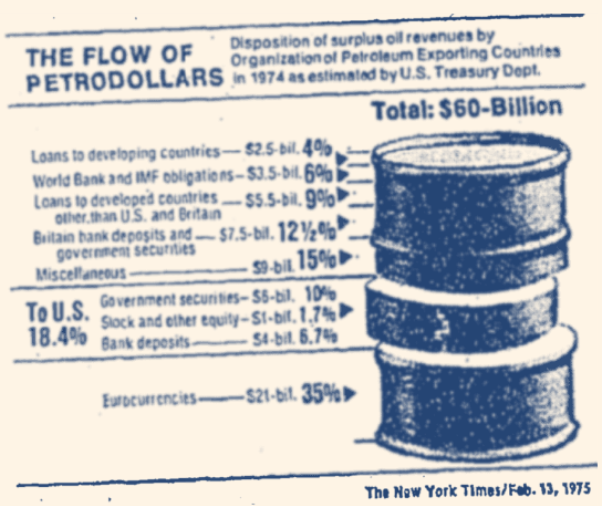

By the end of the year, an estimated 35 percent of $60 billion in Middle East Petrodollar Surpluses went into the Eurocurrency Market, of which the dollar was by far the largest component. 10 percent went to the US Government, 12.5 went to Britain – an unknown chunk, probably most – going to their Government, and 9 percent was lent to governments other than the US and Britain. By 1980, the Saudis had accumulated 12.2 billion of US government bonds, but that only represented about 1.3 percent of the outstanding US Treasury Debt of $930 billion. A good lender at the margin, but not what we would call the lynchpin of the global financial system.

3. After Two Years of Threats…

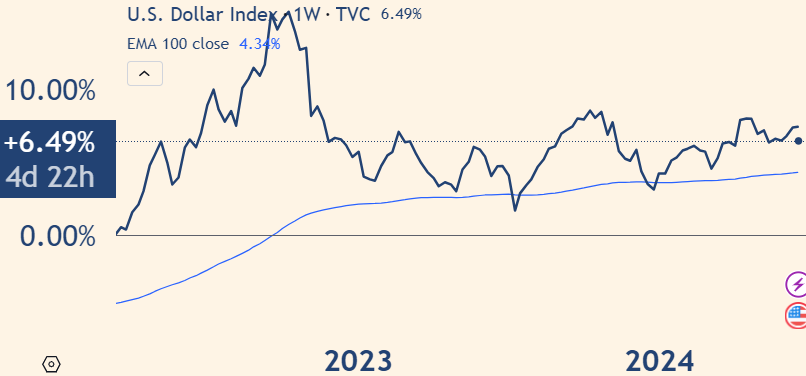

There have been rumblings of an imminent end to the “Petrodollar System” since March of 2022, a couple of weeks after the G-7 countries froze Russia’s Foreign Exchange Reserves. The linked article reports negotiations for China to settle their oil imports in their currency – the Yuan – instead of in dollars. Let’s check and see how currency prices have changed since then.

The DXY index, up 6 1/2 percent since March 2022:

The Yuan/Dollar exchange rate, down 12.6 percent since March 2022

For the last half millennium, the key determinant of which country hosts the global reserve currency (GRC) has been the relative size of that country’s economy. Since China is first runner up to the US, or ahead of it in Purchasing Power Parity terms, the Yuan seems like a natural successor to the GRC position.

That said, a promise by the Saudis to sell oil to the Chinese, for Yuan, does not threaten the dollar’s global position. What makes the GRC what it is, is the fact that it is used in transactions that have nothing at all to do with the host country. While the US makes up a quarter of the global economy, it’s used in 80 percent of trade finance. For a currency to be used in trade finance, there must be vast sums of it available to the international banks to lend. For that to happen, private investment funds and corporations must be willing to store their wealth in that currency. For a currency like the Yuan, or the non-existent “BRICS-buck”, to become the GRC, there must be a seismic shift in the willingness of private entities to hold those currencies. Not just spend them. For an example, look no further than India, where there is so little trust between the I and the R in BRICS that the Russians can’t get their money out of the country.

- Smith, Adam, Paper Money, 1981. The linked PBS article is a reproduction of an excerpt from Chapter 6 of Paper Money, by George Goodman, under the pen name Adam Smith.