Indicators

Interest rates are like all other economic factors in that they are notoriously difficult to forecast.

The path of interest rates is dependent on many variables. The most important are the rate of inflation, the unemployment rate, and the health of the short-term money market. Because interest rates are not objectively set by markets, and are instead arbitrarily set by central bankers, each of these “real” factors must contend with human behavior. In the financial industry this is often dubbed the Federal Reserve’s “Reaction Function”. A great deal of analysis is poured into trying to figure out not only what the economic variables are going to do, but how the people in the Eccles Building (Fed HQ) are going to react.

That said, the two indicators that market practitioners look at to get a “feel” for the path of interest rates are the Federal Reserve’s Summary of Economic Projections and the expectations “baked in” to the prices of two futures markets: SOFR and Fed Funds. Interest rate futures are typically a better indicator because the prices in those markets are arrived at through price discovery – which is to say the chaos of trading – and the people doing that trading have real money on the line. (The people setting the interest rates in D.C. do not).

Summary of Economic Projections – September 2023

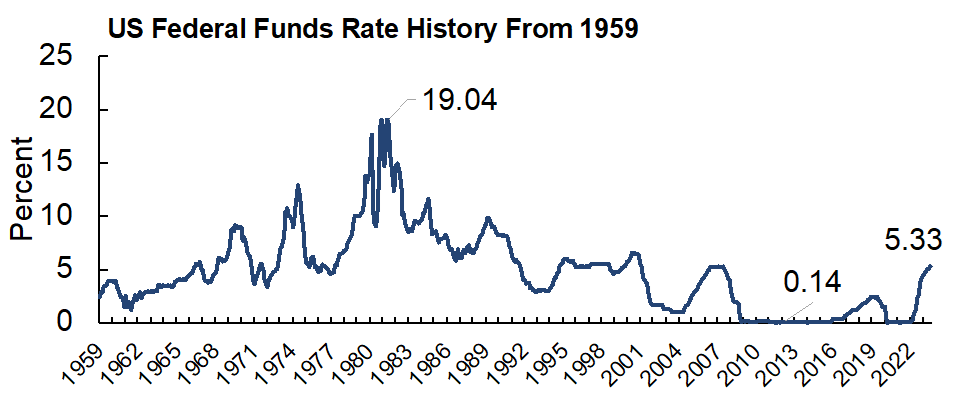

The current target range for the Federal Funds rate is 5.25-5.50. There hasn’t been a new hike since July. The Fed chairman, Jerome Powell, has told reporters repeatedly that he intends to keep rates “higher for longer” until the economic data gives strong indications that the inflation rate is headed down towards two percent. For context, here’s the inflation rate as measured by the US personal consumption expenditures (PCE) price index, and the Federal Funds rate, going back several decades. The main price index that the news cycle and wall street pay attention to is the Consumer Price Index, but we’re looking at “core” PCE because that’s the one the Fed cares about. Most people will look at the PCE figures and think “inflation is way higher than that”, and they would be correct. Most peoples’ grocery bills have doubled in the last three years. PCE doesn’t represent the lived experience of any human being on Earth. We’re only looking at it because it’s the index the Fed likes.

The Federal Open Market Committee (FOMC) posts its expectations about the path of interest rates in their Summary of Economic Projections. These are only released every quarter, not every meeting, so the last one we have is from September.

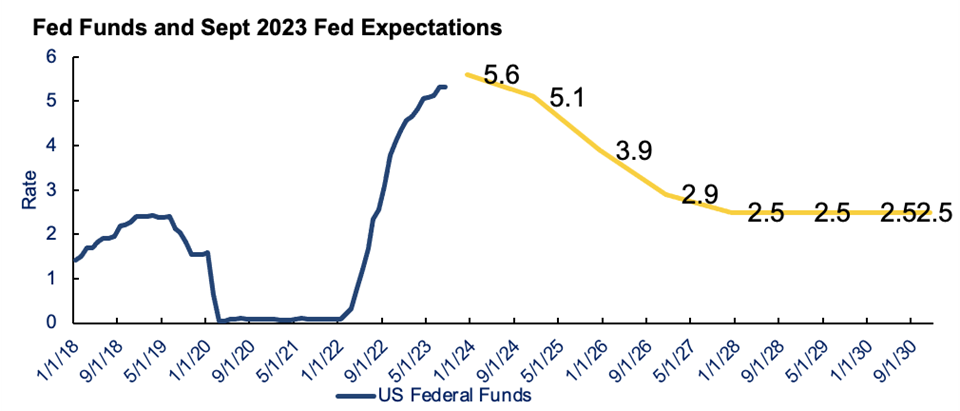

As of the September 2023 meeting the median expectation among the 12 members is for Fed Funds to peak at 5.6 in 2023, which implied one more rate hike of ¼ percent, and then gradually taper off to land half a percent north of their target inflation rate of 2 percent. The Long run interest rate (everything from 2026 onward) indicates what the Fed board members think is the “goldilocks” level for the interest rate – a level that is not stimulating the economy or contracting the economy. Economists have a fancy term for that magical interest rate: “R-star”. Like most theoretical measures that academic economists cling to, r-star doesn’t exist. Nonetheless, they think it’s 2 ½ percent.

We can’t look at the SEP without also acknowledging just how wrong the Fed has been in its path to higher rates. Here’s the most recent expectations for the path of the Fed Funds rate, from the September meeting, compared to that of September and June of 2022. In June ’22 they saw rates peaking at 3.8. In September ’22 they saw rates peaking at 4.6. Yet here we are at 5.33.

But it no longer looks as though the rate will peak at 5.6. The economic projections from September have to be adjusted.

The other irritating thing about the Fed is that they often use certain media outlets to “whisper” to the market, an innovation of the Alan Greenspan era. Greenspan would give speeches hinting at the path of rates leading up to the FOMC meetings, effectively boxing the rest of the committee into whatever path he’d implied. In a way, he forced their compliance.

Nick Timiraos of the Wall Street Journal is widely known to be a sort of “mouthpiece” for Chairman Powell, and on November 14th, he published an article with this sledgehammer of a title:

Cooling Inflation Likely Ends Fed Rate Hikes

- Nick Timiraos and Amara Omeokwe, Nov 14th, Wall Street Journal

Since November 2022 the core PCE inflation reading has gone from 5.09 to 3.67 percent. With this article, Powell is telling markets, “As long as we don’t see an uptick, no more rate hikes”.

That would mean that rates have peaked at 5.33 percent. When would they drop? The average time between the last rate hike and the nearest rate cut is five months. Since the last rate hike was in July, there could be cuts as soon as December. But to get a better feel for that, we’ll look at the other indicator of future interest rates: the futures market. The Futures market may also explain why the Fed has, in the last two months, changed its expectations from one more rate hike to no more rate hikes.

Federal Funds Rate Futures

There is an actively traded futures contract on the Federal funds rate. When traders buy (go long) a Fed Funds Futures contract, they make money when the rate goes down. When traders sell (short) the Fed Funds Futures Contract, they make money when the rate goes up. There’s a Fed Funds contract for each month going out several years. The prices of those contracts at any given time tell us about the market’s expectations of where the rate will go. Unlike the academic economists at the FOMC, these are institutions – banks, non-bank lenders and hedge funds – with billions of dollars on the line. Every major financial corporation has a desk that operates in the markets for interest rate derivatives (the list of which includes Fed Funds Futures). It’s an unavoidable form of risk management.

In a way, the Futures market “knew” that the Fed would stop at 5.33 percent weeks before that article above was published. Back in September the FOMC’s rate expectation for the end of 2023 was 5.6, which meant one more rate hike at some point after July. Well, the futures market expectation was a peak of 5.36 percent in December.

On the other hand, the Futures market doesn’t see the Fed getting down to their forecast of 2 ½ percent in the next four years, either. Futures prices imply a rate only as low as 3.825 percent in mid 2026. Still 1 ½ percent of cuts, but not as much as what the Fed is forecasting.

Futures Traders don’t have a crystal ball, either. A quick comparison of those contract prices from a year ago shows that, like the Fed, the market got it quite wrong as well. The Futures market “saw” rates peaking at 4.3 percent in 2023. And since October, rate expectations have moved down by about a half a percent out to 2027.

In Summary

What should all this mean for your expectations about rates? Both the Futures markets and the Fed are telling us that they expect rates to be lower by the end of 2024 than they are now. The Futures market pricing is for a Fed Funds rate just shy of 5 percent by June. Since the current lower end of the range is 5 ¼, that implies one rate cut in the next seven months.

What’s the risk to that outlook? Two things: direction of the inflation rate and the money market. Higher inflation means higher rates, money market trouble means even lower rates.

Inflation

The PCE inflation rate has not reached the Fed’s two percent target. They’ve indicated through their news whispers (that WSJ article mentioned above) that they are satisfied with inflation moving on a lower trend with each passing month. They don’t need annual inflation to actually get down to two percent to stop hiking rates, they just need to be convinced it’s headed that way. A rise in inflation means pressure for the FOMC to leave the rate where it is, or even go higher.

Money Markets

The money market is where banks and non-bank lenders borrow for terms less than one year, often overnight or only for a couple weeks. When the money market gets in trouble, it doesn’t matter what the Fed had in mind at its last meeting, the Fed is going to cut rates. Leading up to the Great Financial Crisis, Fed Funds peaked at 5.25 percent with the last hike in July 2006. When did the Fed start cutting? Not in March 2008 when Bear Stearns failed, not in September 2008 when Lehman failed, and not in October when Fannie and Freddie went into conservatorship.

The first cut was a ½ percent in September 2007. Why? The money market. In August, the market for a money market instrument called Asset Backed Commercial Paper fell off a cliff, an unexpected victim of subprime mortgage bonds. What pushed it off? A money market fund run by a bank in France – BNP Paribas. The money market doesn’t have borders, trouble in one corner of the world often leads to unexpected trouble in another. The Fed had emergency conference calls in between meetings and began cutting rates in September when the market didn’t recover.

On November 14th, the Fed signaled through its Wall Street Journal whispers that they intend to leave the rate where it is. For Fed watchers, that’s a downshift from their last projection of 5.6 by the end of 2023. I believe that has less to do with inflation and more to do with money markets, not in the U.S., but in the world’s second largest economy, China.

For the last 18 months, most central banks have been on a rate hiking path to fight inflation. Meanwhile, the People’s Bank of China has cut rates. Their one-year lending rate went from 2.9 at the start of 2022 to 2.5 in August 2023. On October 15th, the PBOC unexpectedly lent over a $100 billion to China’s financial system in response to problems in the money market. On October 31st, the interest rate for 7-day loans between Chinese banks reached 50 percent, and in the days since has averaged around 3.6. That doesn’t sound large, but it’s double the PBOC’s 7-day rate of 1.8 percent. If money were as tight in the U.S. as it’s been in China recently, banks would be borrowing from one another at average of 10 ½ percent (double the Fed Funds rate).

While this was happening on the other side of the world, the Fed Funds Futures market reacted. The prices of those contracts are now indicating a rate ¼ percent lower than they were at the beginning of October. For example: the rate expectation for June 2024 moved from 5 ¼ to 5.

Higher inflation is the upside risk for rates, and it probably won’t materialize. A huge source of most of the world’s manufactured goods is China, and that economy is experiencing deflation[1]. The CEO of Walmart said on an earnings call that, “In the U.S., we may be managing through a period of deflation in the months to come… And while that would put more unit pressure on us, we welcome it, because it’s better for our customers”[2]. Home Depot’s CFO told shareholders, “The worst of the inflationary environment is behind us”.

The problems in China’s money market, along with the many mid-sized bank failures in the US earlier in 2023, tell me that rates are headed lower than either of the indicators discussed above would suggest. The Fed expects 5.1 by December ‘24, the futures markets see 4 ½, and that number has been dropping. I view four percent is a realistic rate by the end of 2024, but there is one development that would send it lower. The unemployment level was about 650,000 persons higher in October than it was in July. By one estimate, holiday seasonal hiring is on track to be 40 percent lower in 2023 than it was in 2021[3]. If unemployment continues to increase, the Fed would most likely go into “stimulus” mode with rates. Since they believe the neutral interest rate to be 2 ½ percent, we may see them go as low as two.

[1] “China Falls Back into Deflation…”, Wall Street Journal, Nov 9, 2023. https://www.wsj.com/world/asia/chinas-consumer-prices-fell-in-october-15aa405c

[2] “Deflation Could be Coming…”, CNBC, Nov 16, 2023. https://www.cnbc.com/2023/11/16/deflation-holiday-walmart-ceo.html

[3] Holiday Hiring Demand Drops Off…”, Wall Street Journal, Nov 13, 2023. https://www.wsj.com/economy/jobs/holiday-hiring-demand-drops-off-a-warning-for-the-job-market-7d40e8f4