Summary:

- The Fed’s last projection for the Fed Funds rate, released in September, showed another rate hike to 5.6 percent by the end of the year. The last hike was to 5.25 in July.

- On November 14th, inflation data came in lower than expected. The Fed signaled through its “Fed Whisperer” at the Wall Street Journal that “Cooling inflation likely ends rate hikes” (the headline). That implies the rate has peaked at 5.25, a downshift from the 5.6 forecasted in September.

- Why? Inflation is the cover story. The Fed took its cue from the interest rate futures markets, which started to bet on lower rates in October because of financial problems in the world’s second largest economy, China.

- Crude oil prices took a turn downward at the same time, despite a fresh war in the Middle East. The unemployment count hasn’t seen a new low since April, and this year’s seasonal hiring is projected to be as much as 40 percent lower than 2021.

The Federal Open Market Committee (FOMC) is responsible for setting the key overnight rates in the economy. You and I don’t borrow or lend at these rates, the banks do. Its main policy interest rate, Fed Funds, is the rate banks pay to borrow from one another.

In the 16 months up to July 2023, the Federal Funds rate was hiked from zero to 5.25 percent in the Fed’s effort to fight the highest inflation seen since 1981. In congressional testimony, press conferences, and speaking occasions, Fed Chair Jerome Powell has told the world that he intends to keep rates high until the annual inflation rate gets down to two percent. That’s the official target the Fed set for themselves under Chairman Ben Bernanke in 2012.

The last rate hike came in July, with a quarter percent increase from 5 to 5.25. They left the rate steady at the September meeting, after which they released their quarterly Summary of Economic Projections. Economists are horrid forecasters, so their projections of GDP growth and the unemployment rate probably aren’t worth looking at. But that report does contain the “dot” plot, which shows the median of where they expect the Fed Funds rate to be in the future. The dot plot is a signaling tool, part of what they call “forward guidance”, whereby the committee tries to manage expectations about the path of rates.

In September, the dot plot showed the rate peaking at 5.6 by the end of 2023. That would imply one more rate hike, but fast forward to November, and we still don’t have one.

The annual inflation rate, as measured by the Consumer Price Index, was about 3.25 percent in October, lower than the 8 percent prints seen a year ago, higher than the target. But the month over month reading was a flat zero.

The Fed also uses journalists at the Wall Street Journal to set expectations about rates. In my opinion this practice is juvenile, but it’s what they do. Nick Timiraos is widely known on the Street to be the “Fed Whisperer” of today. In the nineties it was David Wessel. On November 14th, the Fed whispered once again.

- The headline: “Cooling Inflation Likely Ends Fed Rate Hikes”.

- The message: We’re done hiking rates.

- The Street’s interpretation: rate cuts are around the corner, so buy stocks and bonds.

That was a downshift from the expectations set in September. Remember, those projections had Fed Funds reaching 5.6 percent. The article changes that outlook to say we won’t see anything higher than 5.25. Why? Ostensibly, the low inflation print that morning.

But that explanation is the cover story. How do I know? The month over month inflation rate was 0.1 percent in May. Multiply that by 12 months and you get an annual 1.2 percent inflation rate, well below the Fed’s target. That information was known in the second week of June. If this were all about inflation, they could’ve hit the brakes then, but at the next meeting in July, they still hiked Fed Funds by another quarter percent.

Remember in the movie Titanic, when the officers made a point not to tell anyone the ship was guaranteed to sink, because they didn’t want to cause a panic? The Fed is always under the same pressure. If they change the course on rates, it can’t be because something bad is happening in the economy. It has to be something else, a benign cover story. You’ll never hear the Fed chairman say “a recession is imminent”. What’s really going on?

I’ve read dozens of FOMC meeting transcripts, enough to know that one of the first things the committee looks at is what financial markets “expect” them to do.

There are actively traded futures contracts (bets) on the direction of the Federal Funds Rate. Currently there are $1.8 trillion of these contracts outstanding. If you buy or “go long” the Fed Funds contract expiring June 2024, you’re betting the rate will to go down between now and then. If you sell or “go short” the Fed Funds contract with the same expiry, you’re betting that the rate will go up between now and then. Virtually all banks and non bank financial institutions trade interest rate derivatives of this kind. The prices of the contracts tell us something about where “the market” as a whole expects rates to go. Analysts describe this by saying the futures market is “pricing in” x percent of rate cuts, or y percent of rate hikes.

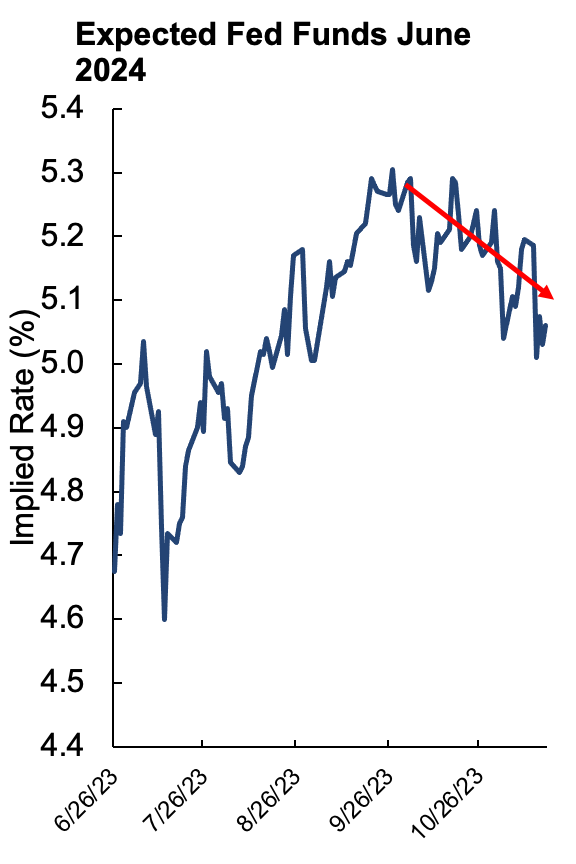

Months ago, the Futures market “saw” Fed Funds reaching 5.3 percent, which would imply no more rate hikes after July. That contradicts the Fed’s projection from September, which we know was 5.6. From October to mid November, the Futures Market downshifted even more, and I’m 99 percent certain that was in response to problems in China’s money market.

The money market is where large companies, both financial and non financial, go to borrow money for terms less than one year. Money markets know no borders. In fact, they often transmit financial chaos from one corner of the world to another. A recent example is the first domino in the Great Financial Crisis of 2008. The Fed started cutting rates not in 2008, but in 2007, months ahead of bank failures in the US. Why? A money market fund managed by a French bank froze up, and that took all of five seconds to throw a wrench into the US money market.

China has a private debt load about 225 percent of the size of its economy. Its Real Estate bubble has been deflating since 2021 and the poster children of that bubble – developers Evergrande and Country Garden – have collapsed in slow motion. The economy is so weak that it has had a negative inflation rate for some months now. In August, this finally started to hit China’s money market. In October, the heat was turned up.

The People’s Bank of China (PBOC, China’s Fed) cut the 7-day lending rate in August to 1.8 percent. Interest rates there have only gone down while the rest of the world has hiked. On October 14th, the PBOC was forced to lend over $100 billion to the money market as its member banks had problems finding credit. On October 31st, the rate for 7-day loans between banks reached 50 percent for some borrowers. Daily average rates have been around 3.6, which sounds low, but it’s double the PBOC’s lending rate. If money were as tight in the US as it is in China, banks would be borrowing from each other at 10 1/2 percent (double the Fed’s rate of 5.25).

In the US, that sent Futures market expectations downward for the first time since March 2023, when several midsized American banks failed. The Fed watches this market like a hawk, there’s no way the committee members didn’t notice. This is why the Fed is signaling a lower interest rate outlook, not the low inflation prints. Below is the rate implied by the June 2024 contract, falling from about 5 1/4 to 5. The rate implied by the December 2024 contract was 4.5 percent as of Friday November 17th. That would indicate 0.75 percent of rate cuts over the next year.

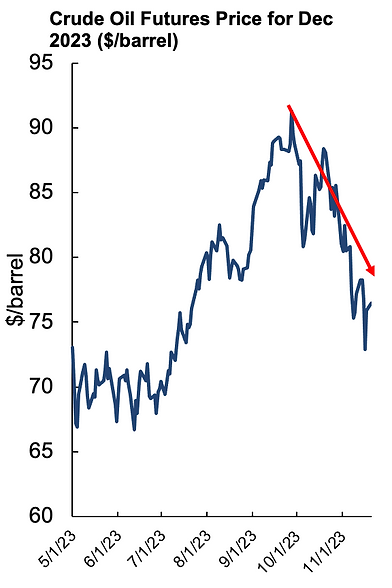

If money market problems persist long enough, large companies have problems borrowing the cash needed to float their operations, which is one of the fastest paths to layoffs. It’s no coincidence that oil prices, another indicator of future economic activity, turned downward at almost exactly the same time as rate expectations. Mind you, this happened in concurrence with the outbreak of a fresh war in the Middle East, which usually pushes oil prices up.

Final thoughts, the ranks of the unemployed in the US haven’t seen a new low since April 2023. The unemployment level is about 850,000 heads higher as of October than it was then. That’s not huge, and could be a noise in the data rather than a signal. But early reports on seasonal hiring for the holidays says it’s a signal. The National Retail Federation estimates seasonal hiring to be up to 40 percent lower this year than it was in 2021.