Introduction

As the dollar enters its second century of dominance as the World Reserve Currency, the sustainability of that dominance is being called into question for the first time in many years. A reserve currency is a medium of exchange (money) that is used for trade, credit, and investment, outside its country of origin. The dollar is by far the dominant RC, as it makes up one side of 90 percent of foreign exchange transactions. That’s 90 percent of a market with $7 trillion of turnover every day. Since other financial systems hold the bulk of their reserves in dollars, it is, in a way, the “base layer” for all the other currencies as well. As Keith Weiner of Monetary Metals puts it, “all other currencies are dollar derivatives”.

“De-dollarization” is an initiative that has surfaced a handful of times over the last half century. Once in 1978, once in 2009, and most recently, in 2022 and 2023, after the G7 froze $300 billion worth of Russia’s foreign currency reserves. Russia and its partners in the BRICS group of nations have egged on this narrative with hints at a gold-tethered settlement currency. With a displacement of the dollar on the table, the question arises, what brought the currency to preeminence and what keeps in there?

Articles with titles like, “Spate of Recent Deals Raises Chatter of a Fading Petrodollar” purport to answer that question. In a word, one of the world’s most important commodities: oil. A surprising number of analysts, money managers and commentators believe that what underpins the dollar’s position in the world is the Petrodollar System. The story goes as follows:

The Nixon Administration’s closure of the “gold window” in August 1971 severely weakened the dollar. Soon after, Saudi Arabia and other oil exporters began to demand gold and other currencies (such as the Deutschmark) in exchange for oil. Sometime around the 1973 oil embargo, the Nixon Administration made a deal with Saudi Prince Fand Ibn Abdel Aziz. The U.S. would sell the Kingdom weapons and other military equipment. In exchange, the Saudis would only accept dollars for its oil exports, which would increase demand for the dollar in the FX markets. We are to assume that all the other gulf states just followed suit, and then everyone just started paying for everything in dollars. Sandstone Capital Management suggests the creation of the Petrodollar System is what cemented the dollar’s position as the Reserve Currency.

The second switchboard in the Petrodollar system controls what the Saudis do with the dollars they accumulate in the oil trade: they “recycle” their surpluses into U.S. Treasury bonds. In other words, the world buys dollars, hands them to the Saudis in exchange for oil, then the Saudis lend them to Uncle Sam. “Petrodollar Recycling”, and again, we are to assume the other Gulf States just followed along.

Are Petrodollars real? A petrodollar is just a dollar spent on oil sold by one of the Persian Gulf States, so petrodollars are real.

Is there a Petrodollar Currency system? This guide will give the key points in the history of the dollar as GRC, and in the process, debunk that myth. Is there Petrodollar Recycling? To an extent, yes. Is Petrodollar recycling what keeps the dollar in its place? The data on petrodollar flows suggest they have no effect on the dollar’s value or even the country’s ability to borrow. There is also evidence to suggest that political “petrodollar recycling” arrangements only pulled capital away from the American private sector since their enactment. The global Eurodollar market, well established by the 1970s, ensured that even if the Gulf States had just parked their surpluses in banks and let the interest roll in, those surpluses would still find their way back out to the rest of the world.

Start of the Dollar System

Was the dollar well-established as the WRC before 1973? Yes, the dollar era didn’t begin in the 1970s, it began in the 1920s. Economist Barry Eichengreen documents the transition away from the pound sterling after World War I in a 2014 paper on International Currencies. The U.S. went from being a net debtor to a net creditor to the rest of the world, and had accumulated about 40 percent of the world’s gold. American savers parked their savings in American banks, which lent to the banks of Europe and South America, which lent to foreign borrowers who were happy to use dollars. Allied governments recycled dollars to pay off their $10 billion of war debt to the U.S., and by the middle of the decade, foreign central banks had more of their reserves in dollars than in sterling. (Eichengreen, Ch. 4).

By 1945, the U.S. had accumulated over two thirds of the world’s monetary gold. The Bretton Woods Agreement of 1944 did not demand that countries hold most of their reserves in dollars, conduct most trade in dollars, or borrow large amounts of dollars. Yet, by the time the agreement was in full effect (1958), foreign nations were doing all of those things anyway. Even America’s arch nemesis, the Soviet Union, had a bank in London and later Beirut so it could transact in dollars.

Did the US/Saudi military relationship start in the 70s? The Saudis agreed to house their first U.S. airbase – Dhahran – in August 1945. It became operational in 1946. The first mutual defense agreement between the two countries was inked in 1951, the first shipment of Walter Bulldog tanks to the Kingdom left the New York harbor in 1956.

1970s – “Petrodollar” Enters the English Language

Was the dollar’s use in the oil market threatened between 1971 and 1973? No, on September 7th, 1973, Peter G. Peterson testified to Congress on “Protecting the dollar and the oil supply”. What’s significant about this testimony is that Peterson titled it, “the Petrodollar Problem” and this is the first time the word “petrodollar” enters civilization. In October 1972, the government had discussed a similar initiative, but without the catchy name.

The Department of State, which has been encouraging Saudi Arabia to invest her growing oil profits in American industry, is interested, as are some oil-security specialists here.

The New York Times, October 2nd, 1972

Several weeks ahead of the ’73 Arab Oil Embargo, what was the Petrodollar problem? At the time, the U.S. had to import about 36 percent of the oil it burned, and that foreign oil was getting expensive. Sending more money abroad to pay for increasingly expensive oil worsened the country’s balance of payments problem. For the previous two decades, Americans had been sending more dollars abroad, in trade and investment, than they received from foreigners. This is called a “Balance of Payments Deficit”, which can threaten a currency’s fidelity if allowed to accumulate. The high oil prices exacerbated the deficits. Peterson’s concern had nothing to do with the Saudis refusing to accept dollars in exchange for oil. Two years after the end of the gold window, the gulf oil states were glad to take dollars. It was a given that the dollar was the currency accumulating in the bank accounts of Arabia’s royal families, hence the very term “Petrodollar”. The goal: convince the Persian Gulf states to “recycle” their financial surpluses from the oil trade into American Assets.

If that seems confusing, think of it as one big subtraction problem. Importing oil means dollars out the door, foreign investment means dollars in the door. If you have too many dollars flying out the door to import oil, get the countries who are receiving all those dollars to send them back in the form of investment. Peterson’s motivations were not altruistic, his goal was to use government to put Arabian dollars together with “American expertise”. As the CEO of the Investment Bank Lehman Brothers, he was going to make money if American diplomats could convince the Saudis to buy American Bonds. Any American bonds. Peterson and his associate, former Under Secretary of State George Ball, sought “to interest the Arabs in a broad range of development projects and to get the United States Government to support the joint development of the Middle East in such areas as food, education, housing, and desalinization”. This summary was produced as part of a 300-page Congressional report on the “Petrodollar Problem” published in Summer 1974.

How U.S. Officials Privately Felt About Gold

While it’s impossible to know everything that happens behind closed doors, we do have one private conversation about the international monetary system from Secretary of State Kissinger and his advisors. On April 25th, 1974, the subject of their concern was the European Economic Community’s (EEC’s) plans to re-monetize gold. Kissinger summarizes for clarification, “They’re putting gold back into the system at a higher price”. An advisor confirmed. “Now that’s what we have consistently opposed”, Kissinger said again for confirmation. To which Thomas Enders said, “Yes, we have, you have convertibility if they – “

“Yes”, Kissinger finished his sentence as if to say, “I understand”. The Nixon Administration would not stand for a return to convertibility. If the Saudis had soured on dollars and had been demanding alternate means of payment during this time, there may have been some concern among these men about selling off of America’s gold stock. There was none. Their objective was to ensure that Europe did not go ahead with re-monetizing gold. As a last-ditch strategy to force their hand, they discussed selling down the country’s monetary gold in order to drive down the price, and “sticking” it with the Saudis:

Enders: The policy we would suggest to you is that, (1), we refuse to go along with this –

Kissinger: I am just totally allergic to unilateral European decisions that fundamentally affect American interests—taken without consultation of the United States. And my tendency is to smash any attempt in which they do it until they learn that they can’t do it without talking to us. That would be my basic instinct, apart from the merits of the issue…

[Later]

Kissinger: So who’s with us on demonetizing gold?

Enders: I think we could get the Germans with us on demonetizing gold, the Dutch and the British, over a very long period of time.

Kissinger: How about the Japs?

Enders: Yes. [Changing countries] The Arabs have shown no great interest in gold.

Kissinger: We could stick them with a lot of gold.

Sisco: Yes (laughter)

Sonnenfeldt: At those high dollar prices. I don’t know why they’d want to take it.

The EEC’s monetary ambitions collapsed that year. The U.S. held onto its gold stock, still valued at the last peg of $42 an ounce. At the official price, it’s worth $11.037 billion, at the market price, it’s worth about $523 billion. At a time when Western Europe was seriously considering the re-monetization of gold, the U.S. Secretary of State was joking about “sticking” the Saudis with some of America’s stockpile. Only a couple of years after the closure of the gold window, retaining the gold stock was not a concern.

Petrodollar Recycling

While the Saudis were partial to gold in the early stages of their economic relationship with the U.S., there’s no indication that it was their priority in 1971. In the 1930s, the Saudis demanded a four-gold-shilling royalty on every ton of oil. From 1950 onward, the royalty was increased to half of all profits, which were now in dollars. This was a steep increase, but did not protect the Saudis from a devaluation as a gold-shilling-royalty would. After the end of the gold standard, Western oil firms did have negotiations with the Governments due to the dollar’s depreciation, but they had nothing to do with the currency oil would be sold for. To adjust for drops in the dollar’s value, the gulf states negotiated for price increases. Those price increases were in dollars. Perhaps the gulf state governments were making those price demands based on the market price of gold, but it’s more likely that they were responding to the abnormally high inflation that was hitting the entire world at the time. Saudi Arabia’s inflation rate was 4 percent in 1972 and 16 percent in 1973.

Is there any validity to the Petrodollar System idea? Yes, the second switchboard known as Petrodollar Recycling, first coined by Peter G. Peterson in 1973, was realized in 1974.

In 2016, Bloomberg News won a Freedom of Information Act Request filed on the Treasury department, demanding the release of data showing Saudi Arabia’s holdings of American debt. In the preceding weeks, Republicans had introduced a bill to investigate Saudi Arabia’s involvement in the 9-11 terrorist attacks. In response, a prominent Saudi official told reporters that the Kingdom could sell $750 billion of U.S. assets. This inspired a rare action of real journalism among today’s media to sue the government for the truth. The FOIA request was for data on Saudi Arabia’s ownership of US Treasuries over the last several decades. The record begins in 1974.

In July of that year, Treasury Secretary William Simon flew to Jeddah to negotiate with finance minister Prince Fand Abdul Aziz. According to Bloomberg, Simon made a deal with the Saudis whereby the U.S. would provide weapon sales and technological assistance. In exchange, they would “recycle” a large amount of their trade surpluses – a result of the high oil prices – by buying U.S. government bonds. One of the conditions was anonymity, as Saudi Arabia could not be seen lending to Israel’s biggest ally. The Saudis’ purchases were anonymous de jure, maybe, but practically public, de facto. When the Treasury published its International Capital Reports, it lumped all of the holdings of the Gulf States into a single category. With Saudi Arabia being the biggest of the pack, only an idiot would believe the holdings in this category did not include theirs. There is one reason to doubt the accuracy of Bloomberg’s narrative. Secretary Kissinger promised enhanced military development as part of an agreement to get more oil out of the Saudis only a few months earlier. How much sense does it make that Nixon’s Administration was able to play the same card again in July? Since Simon himself died in 2000, we may never know exactly what the U.S. contributed to this arrangement. But because the record of Saudi US debt holdings starts in 1974, we can be quite certain that their contribution was to buy bonds.

The Impact of Petrodollar Recycling

The question is, just how consequential is Petrodollar recycling? How dependent is the U.S. on the credit of the gulf states and therefore, the continued funding of the Saudi military? Incidentally, that is another misconception. The Saudis don’t receive American-made weapons as foreign aid, the way Ukraine did in 2022 and 2023. Ever since that first shipment of Walter Bulldogs in 1956, the Kingdom has paid for the weapons it gets from the United States. The amount of true foreign aid spending on the country is minimal.

For instance, Saudi Arabia and U.A.E. agreed to spend $5 billion on American weapons in August 2022. Meanwhile, neither country cracks the top 15 list of foreign aid recipients for that year, the lowest of which got $750 million from the U.S. In 2021, They received less than $5 million combined.

In a way, both America’s contribution and Saudi’s contribution to William Simon’s “Recycling” deal benefit America. The U.S. gets to buy oil with printed money, the Saudis then send the money back in exchange for weapons, then when they have enough weapons, they send it back in the form of bond purchases. A good deal, but again, just how much does the dollar depend on it?

Even with no evidence, let’s suppose that there were a petrodollar currency agreement in addition to Bloomberg’s dubious petrodollar recycling agreement. Suppose that both began in 1974, coincident with the Saudis buying loads of Treasuries. This is the policy that supposedly cemented the dollar’s position as the world’s top reserve currency. If this is how events unfolded, we would not expect to see the dollar reach its lowest point of the decade several years after such a policy began.

In 1978, the dollar index fell 17 percent, hitting a low it would not break through until 2008. For the first time ever, the U.S. Treasury issued bonds denominated in foreign currencies. “Carter Bonds” were two-and-four-year notes denominated in Swiss Francs and Deutschmarks. In Summer 1978, the gulf states did convene a meeting of finance officials to discuss diversifying their currency holdings. The resulting proposal was to use a “basket” currency issued by the International Monetary Fund, the Special Drawing Right (SDR). SDRs were 33 percent weighted to the dollar at the time.

Ultimately, that conversation died out and no action was taken. A 1986 paper from the Bank for International Settlements showed that there was no diversification of foreign currency reserves, away from dollars, in the late 70s.

By 1979 the dollar was trading sideways[1] and its rapid depreciation was no longer concern. The Gulf states abandoned their SDR reserve plans. Was it pure economics? No, it would be naïve to think the Gulf States could buck the dollar without consequences. But if these governments had really pegged their defense capabilities to a promise to keep taking dollars for oil, why would they hold a multinational conference to discuss ending their part of that deal?

The first “Volcker Shock” pushed dollar interest rates from 14 to 20 in Spring 1980. With another interest rate shock from 10 to 22 percent in the latter half of that year, the dollar finally rebounded. While Reagan favored too large of a government and too large of a debt burden for my political principals, I cannot leave out the following detail. Of all major political and economic events of that time, the election of President Reagan in 1980 corresponds closest with the rally in the dollar.

Key points in the Great Inflation and the US Dollar DXY Index

1.Nixon “temporarily” suspends convertibility to gold, August 1971. 2. Treasury Secretary William Simon reaches “Petrodollar Recycling” Agreement with Saudis (According to Bloomberg), July 1971. 3. Gulf State Finance Ministers convene meetings to discuss diversification out of dollars, July 1978. 4. First Interest rate shock, March 1980. 5. Ronald Reagan wins the presidency, American hostages let go in Tehran, November 1980. 6. James Baker appointed to head Treasury Department, January 1985. 7. Plaza Accord, September 1985.

Why was the dollar’s reserve status the most threatened in its history a few years after the deal was enacted? The most likely answer is that there is no Petrodollar currency agreement holding the system in place. Moreover, the Arabs’ American debt purchases have never been a large enough force in the monetary system to make or break the dollar.

If petrodollar recycling were the gravity holding the dollar system together, we would expect to see a price response in the dollar if the Gulf States stopped buying US Treasuries. If they didn’t buy any new Treasuries for -say – over 20 years, we might expect another dollar crisis. But according to that record published in 2016, the Gulf region was a net seller of U.S. debt from 1983 to 2004. Saudi Arabia’s Treasury portfolio has fallen by 30 percent since December 2019 yet the dollar is 7 percent higher than it was then.

Saudi Arabia’s holdings of U.S. Treasury Securities, in billions, 2012 to 2022

Source: Treasury International Capital Report.

By 1981, the dollar crisis had come and gone. Forty years later, the Gulf States still sell their oil for dollars, they still deposit their surpluses in European and American banks, and the dollar is higher than it was in 1978. By 1984 the currency was printing new all-time highs. The dollar index peaked in February 1985. The reversal is most closely correlated with the appointment of James Baker as Treasury secretary in late January. That September, officials from the G5 governments signed the Plaza Accord, which is almost universally credited for bringing the dollar back down.

And this “boomerang” illustrates the ultimate problem of the reserve currency. While the dollar is not in danger of losing its reserve status to the BRICS or any individual member of the bloc, that doesn’t mean having the GRC is a good thing. French President Charles De Gaulle’s Finance Minister called the reserve status America’s “Exorbitant Privilege” in 1965 (Eichengreen, 4). His economic advisor Jacques Rueff believed that the Fed was a major obstacle to French economic progress because of its policy of manipulating interest rates. Six years earlier, Polish Economist Robert Triffin testified before Congress on why being host to the GRC is a double-edged sword. Though an important insight, he articulated it in a very “Keynesian” way that I believe he is given too much credit for…

The Costs and Benefits of Reserve Currency Status

The issuer of the reserve currency is supplying the reserves on which the rest of the world’s currencies are based. Its IOUs are everyone else’s asset. The rest of the world [according to Keynesian dogma] has to have a growing monetary reserve for its economy to grow, but that requires the U.S. to keep issuing IOUs. As the U.S. keeps issuing IOUs, its solvency as the reserve currency issuer is called into question. The reserve issuer (the U.S.) is destined to run larger and larger deficits as the rest of the world demands its IOUs, until there’s a run on the gold stock. This testimony was one year after the Bretton Woods “System” began, the first year that central banks could return dollars to the Fed in exchange for gold (though most didn’t).

Another interpretation of the Triffin dilemma is that America’s main export to the rest of the world is debt, but the rest of the world can’t buy our debt with their money (because we have no use for their money), and so the only way they can pay is with goods. Some say that this, more than anything else, has caused a “hollowing out” of America’s manufacturing base. Overseas labor and capital are made relatively cheaper when your currency is strong, so your businesses spend on overseas capital and labor.

The Triffin dilemma misses half of the problem; it covers the dollar’s role as the global reserve, not the dollar’s role as credit. It leaves out the consequences of dollar strength and weakness. Because the dollar is what’s saved, it’s also the currency in which the most cross border loans are made. Since the 1920s and, to a much greater extent, the 1960s, corporations and governments all over the world have borrowed trillions of dollars. As of Q3 2023, there was $13 trillion in (known) cross border dollar debt, and an estimated $80 trillion in dollar payment obligations in the form of foreign currency swaps and forwards. These derivatives can be used to do the economic equivalent of lending dollars across borders without the borrower incurring what regulators consider to be a “loan”.

On the credit side, everyone else in the world has dollar-denominated payment obligations, which means they need to regularly buy dollars. What happens when the dollar gets too strong, as it did in 1985? They cry uncle. And often, there’s a full-blown currency crisis, as began in Emerging Markets with the dollar’s rally in the early 80s.

On the reserve side, everyone else in the world is holding dollar assets, mostly the bonds of the U.S. Government and Government Sponsored Enterprises. What happens when the dollar gets too weak? The Gulf State finance ministers convene a meeting over whether or not to keep investing their oil revenues in your economy. Or the Chinese blast your economy as unstable and motivated by greed at a conference of the G20, as happened at another dollar low point in 2009. This is the bite of reserve status. Foreign institutions can’t stand a dollar that’s too weak because that means the values of those reserve portfolios of US securities fall. In the gold standard days, this would be like if some of your country’s gold fell into the ocean whenever the dollar got weaker. There is an offsetting force, though, as a weaker dollar usually means more dollars are flowing outside the U.S. That effectively increases the “gold” stocks of the foreign central banks to some extent. And so, the global financial system continues to have “hiccups” as it is pulled between strong and weak dollar conditions. Those conditions are ultimately determined by what central banks do with their interest rates and where capital is flowing in the credit markets. Every other country in the world has a stake in what the Federal Reserve decides Fed Funds will be this month, and how much money the American banking system pumps out in a given quarter.

What is the benefit? The more demand there is for reserve assets, the more foreign investors will bid up the prices of those financial securities. When bond prices go up, their yields decrease, and American corporate and government borrowers get to pay lower interest rates than they otherwise would. How much lower? It’s estimated that American borrowers can borrow from the rest of the world at a rate two to three points lower than the rate at which it can lend to the rest of the world. In a way, the U.S. gets to be a bank. Both the private sector and the government sell their IOUs to the rest of the world, another way of saying “take the world’s deposits”, and then they lend the deposits out at a rate two to three percent higher. This exactly the business model of a plain vanilla commercial bank… except when this bank wants more reserves it can just print them. Then, like a boomerang, some of that money comes right on back as deposits from the rest of the world. Under a gold standard, those stacks of mostly idle gold bars sitting in vaults acted as a limit on the size of the reserve. That put a governor on the rate of growth in the system as a whole. With no tethering at all, the reserve can be expanded or contracted at will.

While there’s some logic in the idea that the dollar’s reserve status is derived from its ability to purchase oil, the same way that it used to be derived from its ability to purchase gold, the data just doesn’t support that version of history. Dollars were gladly accepted for oil before 1974, they were gladly accepted during and after 1974, and with the exception of a multilateral government meeting in 1978, this hasn’t changed. The Saudis kept only 13.5 percent of their reserves in gold (compared to 81 percent in foreign exchange – mostly dollars). Their central bank was not even the uncooperative one that forced the U.S. to payout gold in 1971. That was France. What was the most important point in the dollar’s path to reserve status? The international banking system tends to make loans in the same currencies it gets deposits in. For there to be dollar lending outside the U.S., the U.S. economy would have to consume less than it produced. It would have to be a capital exporter, a net lender, to the rest of the world. By 1920, it was. The U.S. maintained an open capital market, which means foreigners can both put money into and take money out of U.S. banks and brokerages with relative ease. This was not true of Britain from 1939 to 1980, the same period that the Sterling share of global foreign exchange reserves fell from 90 percent to 5 percent. (Eichengreen, pg. 119). It is not true of China, Russia, or India.

Just as the oil trade did not make the greenback, it will not break the greenback. That’s not to concede that de-dollarization of the global oil markets is imminent, but to say that given the evidence, the dollar can withstand a few oil deals between the Saudis and BRICS members.

What makes the reserve currency is, as the word “reserve” suggests, not what money the world trades in but what money the world saves in[2]. With that in mind, what happens if the Saudis take Chinese Yuan for Liquid Natural Gas, as they agreed to in 2023? For the Saudis, this works out as a dollar preservation policy. The country imported $30 billion of goods and services from China in 2021. Any Yuan deposits that Saudi Arabia receives for those LNG exports will be forwarded right back to the Chinese in payment for those imports. Thus, the Saudis get to preserve their dollar reserves instead of using them to pay for China’s products. China also benefits because it doesn’t have to buy the dollars for some of its imports, but it will lose the potential increase in dollar reserves if the Saudis pay for goods in Yuan. All of these actions having been taken, is the structure of the world’s reserve really changing? No, the Saudis are only taking in amounts of Yuan that they intend to send right back to China. The Russians are finding out the hard way what happens when one country holds more balances of another country’s money than it needs in order to settle trade.

In February 2023, a great deal of noise was made when Russia sold oil to India in exchange for the currency of the United Arab Emirates, the Dirham. Interestingly, none of the reporting on this mentioned that the UAE currency is pegged to the dollar. Managing a currency peg means, without getting into the gritty details, that the more there is demand for the Dirham, the more dollar reserves the UAE’s central bank will buy. Saudi Arabia and the five other Gulf Cooperation Council (GCC) countries have their currencies pegged to the dollar and no reported intention to change.

Similarly, it seemed to be a big deal when India began paying for larger quantities of Russian oil in Rupees instead of dollars. Another step on the path to a commodity-backed “BRICS” currency, so it was thought. Instead of strengthening the Rupee, the plan revealed the lack of trust within this supposed currency union. Months later, in May 2023, the Russians were pushing India for concessions on its capital controls. Turns out, the country has long maintained strict rules about what non-Indians can do with bank deposits of Rupees, so all of Russia’s oil revenues from India are sitting idle in Indian banks. Russia prefers that the Indians pay in Yuan, but that preference only came after they were (supposedly) exiled from the dollar financial system.

The last factor in the viability of a BRICS currency is the past experience of government-engineered “basket” currencies in and of themselves. The first basket currency was introduced by the International Monetary Fund in 1968. It was the SDR – Special Drawing Right – backed by many different reserve currencies and pegged to gold. Have any private groups ever demanded the ability to use SDRs? Have international banks lent money to governments in SDRs? Has it facilitated any process other than as a unit for bookkeeping? No.

For a currency like this to be successful, masses of entrepreneurs, investors and creditors would have to (a) understand what a currency basket was and (b) entrust the safety of their financial assets to the governments of the BRICS governments. It simply is not enough for a government to promise a gold-pegged currency if that government has no credibility. The US dollar itself was redeemable for specie, for 130 of the first 143 years of the country’s existence. It didn’t become a reserve currency until the tail end of that period. The U.S. “Bank” had to offer gold convertibility as well as trust and security. Having borders far away from the combat zones of the first and second World Wars helped. Russia’s central bank may offer to buy gold for rubles, but if a sizeable chunk of the global investment community doesn’t trust Russia with its savings, their reserve status isn’t going to improve.

The Importance of Price Response

Russia has a $40 billion equivalent trade surplus with India, but can’t spend the excess income it’s getting because India doesn’t make everything Russia wants to buy. The Saudis settled a contract for Liquid Natural Gas delivery with China in Yuan in 2023. Meanwhile, Russia and China have removed dollars from 90 percent of trade settlement between the two. The last point to be made is on the “dollar doom” predictions that usually follow from the belief in the supposed Petrodollar System. There is de-dollarization is in progress, to the extent that some countries were forced to accelerate it by policy and economic circumstance. The questions are what effect it will have on the economy and what effect it will have on dollar assets. For the dollar doom predictions, those in which inflation reaches double digits and the government pays 20 percent interest on its debt, to come true, prices must eventually agree.

Russia and China have de-dollarized their foreign exchange reserves since 2015, the year Russia grew one step closer to conflict with the U.S. due to the Euromaidan Revolution in Ukraine. For China, it was the peak of foreign investment flows, the peak in the value of its currency, the peak in its stock market, and the peak in its economic growth rate. In 2020, De-dollarization had been in progress for 5 years, and yet, Uncle Sam’s 30 year interest rate reached an all-time low of 1.15 percent. Despite two years of high inflation, reaching 9 percent, foreign governments are still lending the U.S. government money at a 30 year rate of 4.2 percent. In February 2024 that is a whole percentage point below the overnight interest rate set by the Fed.

The US 30-year Treasury Yield from 2015 to present.

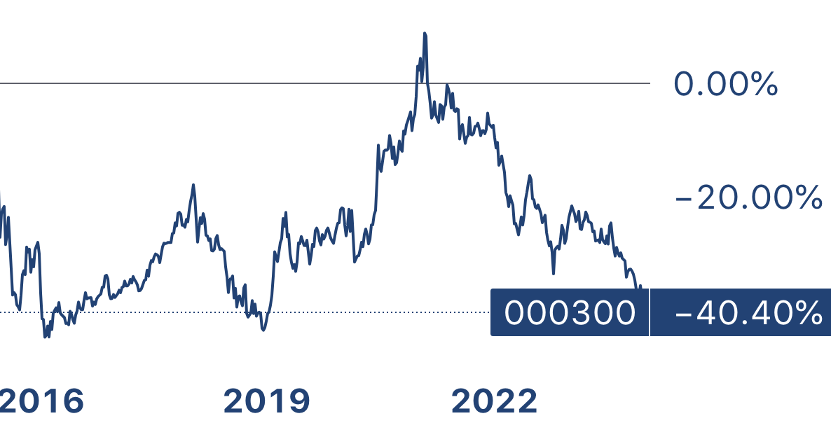

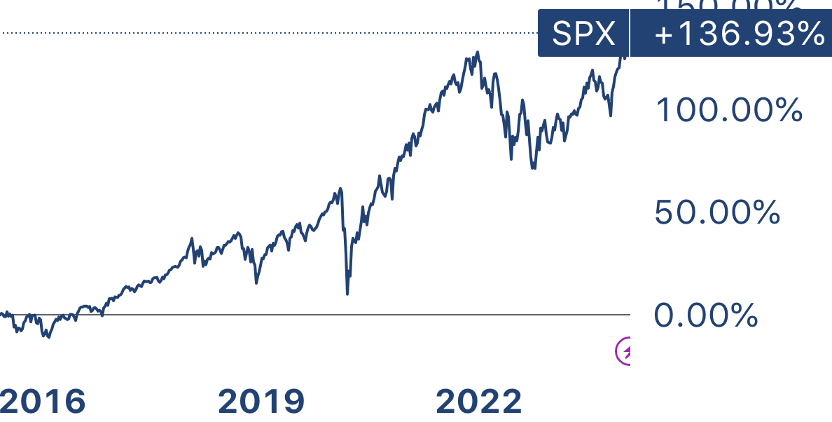

The key BRICS assets have not fared well over the same period. Since June 2015, the Ruble is down 41 percent, the Yuan is down 13.7 percent, and the Chinese stock market is down 40 percent. The U.S. stock market is up 137 percent.

Percentage change in the dollar value of the Ruble since June 2015.

Percentage change in the dollar value of the Yuan since June 2015.

CSI 300 Chinese Stock Market Index from June 2015.

The S&P 500 stock index from June 2015.

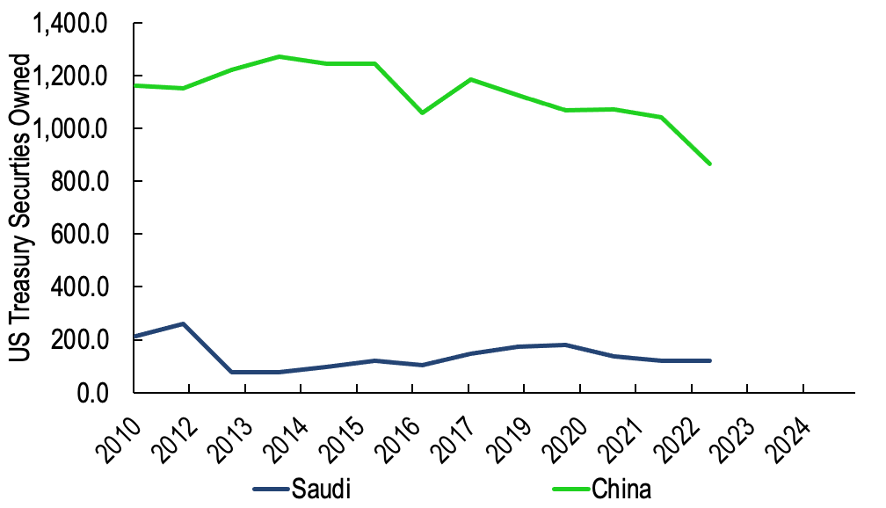

Finally, investors have to understand the concept of “Forced” De-dollarization. Having followed this subject for a long time, I regularly see a tweet showing China’s net decrease in US government bond investments since 2015. It is used as evidence that the “East and South” will dump the “West” to the West’s detriment. The chart out of Saudi Arabia looks similar, with a net decrease of 33 percent since 2019. As mentioned earlier, the Saudi Riyal is pegged at a rate of 3.75 to the dollar. Unless they end the peg, then if the Saudi Central Bank is selling reserves, that means there is pressure on the Riyal and they are having to prop up its value.

Foreign Exchange Reserves Held in US Treasury Debt by China and Saudi Arabia, from 2010

Source: Treasury International Capital Report

The Chinese run a “soft” peg to the dollar; its value has been allowed to steadily decrease from a 6:1 ratio to a 7:1 ratio since the mid 2010s. If the currency is falling, coinciding with a decrease in reserves, it’s a strong indication that the central bank is selling reserves to cushion the fall in the currency.

At some point, the U.S. dollar will become a less significant currency. It will probably happen over the course of a decade. That’s about how long it took for the pound sterling to go from making up ninety percent of global FX reserves to making up less than five. The resulting damage depends on the reason for the loss of market share. Does the U.S. lose the top position because another economic power gradually takes over its share of trade and investment? Or does it lose the top position because it has a debt burden three times the size of its economy and no productive capacity? Those factors will determine what the adjustment is like for those inside the U.S. economy. In either scenario, the prices will indicate what’s going on. The dollar will become weaker against its successor, not stronger. US assets will underperform as the world’s savings flows into the new reserve assets. We will not see the DXY up 30 percent on a 10-year basis. Whatever currency ends up taking the mantle, it will not have been down 16 percent on a 10-year basis against the “legacy” reserve currency, as the Yuan is today.

Source Guide

A guide to all of the sources that were part of investigating the existence of a petrodollar system:

“The Global Foreign Exchange Market in a higher-volatility environment”, the Bank for International Settlements, December 2022, https://www.bis.org/publ/qtrpdf/r_qt2212f.htm

“Kremlin says it has list of Western assets to be seized if Russian Assets are confiscated”, Reuters, December 29, 2023, https://www.reuters.com/world/kremlin-says-it-has-list-western-assets-be-seized-if-russian-assets-are-2023-12-29/

“Spate of Recent Deals Raises Chatter of Fading Petrodollar”, Forbes, April 2023, https://www.forbes.com/sites/davidblackmon/2023/04/02/a-spate-of-recent-deals-raises-chatter-of-a-fading-petrodollar/?sh=3d25ea585964

“The Rise of the Petrodollar”, Sandstone Asset Management, January 2018, https://www.sandstoneam.com/insight/rise-of-the-petrodollar

International Currencies, Past Present and Future: Two Views from Economic History, Barry Eichengreen, Bank of Korea Working Papers, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2580651

(Compositions of Foreign Currency Reserves on pages 6 and 12, of public debts on page 10, and of oil imports on page 11)

Exorbitant Privilege: The Rise and Fall of the Dollar. Eichengreen, Barry. 2012. Oxford University Press. Page 4.

International Currencies, Past Present and Future. Eichengreen, Mehl, and Chitu. Princeton University Press, 2017, https://www.amazon.com/How-Global-Currencies-Work-Present/dp/0691177007

(Chapter 4)

The Moscow Narodny bank was widely known for settling trade in, and lending, dollars to firms and municipalities in Britain. “British Municipalities Widening their Use of Foreign Financing”, March 1964, the New York Times. https://www.nytimes.com/1964/03/16/archives/british-municipalities-widening-their-use-of-foreign-financing.html?searchResultPosition=6

The Moscow Narodny bank was widely known for settling trade in, and lending, dollars to firms and municipalities in Britain. “London shift set by Moscow bank; business expansion prompts move to larger offices”, February 1964, the New York Times. https://www.nytimes.com/1964/02/06/archives/london-shift-set-by-moscow-bank-business-expansion-prompts-move-to.html?searchResultPosition=4

The Moscow Narodny bank in London is directly named in one of the two origin stories of the “Eurodollar” market. According to Adam Smith (pen name of George Goodman), Narodny maintained dollar balance to settle trade in wheat and oil, and made the first Eurodollar loan of $800,000. https://www.pbs.org/wgbh/commandingheights/shared/minitext/ess_currenciesfloat.html.

The USSR’s Moscow Narodny bank was widely known by the early sixties for settling trade and making loans through its London headquarters in dollars. By 1963 they would get more for it from a private sale in the Middle East than from Western official institution at the fixing price of $35/oz. The gold was used to fund a major wheat purchase in dollars. “Soviet Bank Unit Opened in Beirut… Seen as Possible Outlet for Russian Gold”, Oct 1963, the New York Times. https://www.nytimes.com/1963/10/22/archives/soviet-bank-unit-opened-in-beirut-soviet-bank-in-beirut-is-seen-as.html?searchResultPosition=3

The Dhahran airfield was operational in 1946 and remained so until 1962. “U.S. Builds Big Airfield in Saudi Arabia for Use by the Military for three years”, February 8, 1946. The New York Times. [The U.S. Air Force would stay at Dhahran until 1962] https://www.nytimes.com/1946/02/08/archives/us-builds-big-airfield-in-saudi-arabia-for-use-by-the-military-for.html?searchResultPosition=8

The first mutual defense agreement between the U.S. and Saudi Arabia was signed in 1951. “Foreign Relations of the United States, 1951, the Near East and Africa”, Volume V, Office of the Historian, Department of State. https://history.state.gov/historicaldocuments/frus1951v05/d591

The first shipment of tanks to Saudi Arabia caused a scandal for the Eisenhower Adminstration. “Tanks for Saudi Arabia: A Tangled U.S. Episode”. February 1956. The New York Times. https://www.nytimes.com/1956/02/26/archives/tanks-for-saudi-arabia-a-tangled-us-episode-deal-long-in-the-making.html?searchResultPosition=7

Peter G. Peterson suggests gulf states invest dollar oil revenues into American securities and projects in exchange for US government economic and military assistance. “Congress Gets Plan to Protect the Dollar and Oil Supply”. September 1973. The New York Times. https://www.nytimes.com/1973/09/07/archives/congress-gets-plan-to-protect-dollar-and-oil-supply-need-to-balance.html?searchResultPosition=1

The U.S. balance of payments in the late 40s and 50s. “The United States Balance of Payments from 1946-1960”. Monthly Review, Vol. 43 No. 3. March 1961. The Federal Reserve Bank of St. Louis. https://fraser.stlouisfed.org/files/docs/publications/frbslreview/rev_stls_196103.pdf

“U.S. Balance of Payments Policy in the 1960s”. Eichengreen, Barry. May 2000, NBER Working Papers Np. W7630.

Some details about oil imports (36%) and production in the early 70s. “How an oil shortage in the 1970s shaped today’s economic policy”. May 2016. NPR. https://www.marketplace.org/2016/05/31/how-oil-shortage-1970s-shaped-todays-economic-policy/.

From 1971 to 1973 there were multiple Geneva Agreements between the Gulf States and Western oil firms (Aramco in Saudi Arabia) to adjust for depreciation in the dollar. The Gulf States negotiated more room to increase the oil price as the currency got more volatile. The governments were also claiming about half of profits in taxes. They accepted dollars. “The Economy and Finances of Saudi Arabia”. January 1974. The International Monetary Fund. https://www.elibrary.imf.org/view/journals/024/1974/002/article-A001-en.xml

“A new force has arisen on the monetary scene – the power of oil money in North Africa and the Middle East”. On March 15th a $2.7 billion flood of cash overwhelmed the German foreign exchange market and forced the closure of the exchange for the day. A German monetary official guessed half the money that came in was from central banks, and half of that was from the Middle East.

This article in the November 1990 Federal Reserve Bulletin details the foreign exchange interventions the U.S. performed in response to the 1978 dollar crisis. For the first time ever, the government issued bonds in foreign currencies and accumulated reserves in foreign currencies. “U.S. Exchange rate policy: Bretton Woods to Present”. The Federal Reserve Bulletin, November 1990, page 900. https://fraser.stlouisfed.org/files/docs/publications/FRB/pages/1990-1994/32648_1990-1994.pdf

Eurodollars and their use in the American banking system. “The Eurodollar Market in the United States”. Marco Cipriani and Julia Gouny. May 2015. Liberty Street Economics. https://libertystreeteconomics.newyorkfed.org/2015/05/the-eurodollar-market-in-the-united-states/

Observatory of Economic Complexity – China and Saudi Arabia. https://oec.world/en/profile/bilateral-country/chn/partner/sau

Robert Greene on why the BRICS are not ideal candidates for reserve currency status. The issues discussed are the countries’ closed capital accounts, the volatility of their currencies, and cost of convertibility to Emerging Market currencies because of the lack of financial infrastructure. In a referenced paper, Eichengreen, et al. argue that the Chinese do not need to liberalize their Capital Account for the Yuan to grow in international importance. In the same article, the argue that because the Chinese will have to hold a stable stock of dollar reserves to establish credibility, internationalizing the Yuan will sustain demand for dollars, rather than crashing it. https://carnegieendowment.org/2023/12/05/difficult-realities-of-brics-dedollarization-efforts-and-renminbi-s-role-pub-91173

Michael Pettis, Professor at Peking University, argues that the Chinese would have to offer foreigners an open capital and current account, removing its capital controls. https://carnegieendowment.org/chinafinancialmarkets/86878

Composition of Official Reserves, The International Monetary Fund, https://data.imf.org/?sk=e6a5f467-c14b-4aa8-9f6d-5a09ec4e62a4

[1] Which is to say, “the price is moving with little or no trend”.

[2] A paraphrasing of Economist Warren Mosler from a 2022 interview on the subject.