In 2021 the cracks in China’s real estate sector were exposed when its biggest developer – Evergrande Group – started having trouble making interest payments on its debt. The company’s bonds were never in amazing shape. Junk debt, to be sure. They traded around 83 cents on the dollar in May of 2021, but by December they traded at 15, and in October 2023, they traded around 2 cents.

As Evergrande unraveled, American analysts dubbed it China’s “Lehman moment”. That was a reference to September 2008, when the American investment bank Lehman brothers saw its stock plummet to zero. That event is incorrectly – but widely – considered to be the beginning of the Great Financial Crisis. The tanking of China’s real estate sector has proven to be a slow burn. Two years later, major developer Country Garden and now a large trust company are embroiled in the mess. It is now known that China’s Trust companies have large exposures to the fall in property values; Zhongzhi may just be the first domino.

What if China is not in the midst of a Lehman moment, but a Knickerbocker moment? The Panic of 1907 began with a run on the Knickerbocker Trust on October 18th of that year. It was a proper shadow banking meltdown, in which run-of-the-mill banks were not the primary culprits. So far, the faces of China’s unfolding financial crisis have not been banks, but non-bank companies doing high finance. On November 27th the Wall Street Journal characterized it as a “Looming shadow bank meltdown”. There are many parallels.

Trust companies are practically nonexistent in American finance today, but they made up a large chunk of the business in the 1890s and early 20th century. They were non-bank banks, what we now call “Shadow Banks”. Just like banks, they offered deposits. Unlike banks, the deposits paid higher rates of interest, and were used to invest in fun assets like the stocks and bonds of railroads and other industrial firms.

Trust companies are now a popular source of financing in China. The industry is about 3 trillion dollars in size and, just as American railroads depended on trusts to float their bonds in the early 20th century, China’s developers have depended on trusts for cash flow in the last several years.

The modern trusts don’t offer deposits, per se, they offer something that’s economically the same with a different name. Wealth Management Products – WMPs – fancy time deposits that promise higher interest rates than bank accounts. Zhongrong International and others sold WMPs to households and used the proceeds to invest in China’s real estate boom. Some were limited to wealthy investors, with minimums like $420 thousand. Others, not so limited. Zhongrong’s products offered returns of 7 to 8 percent. Others offered 12 to 13. The People’s Bank of China has its deposit rate set at 1.5 percent, which means the average household is getting a lot less on a regular savings account.

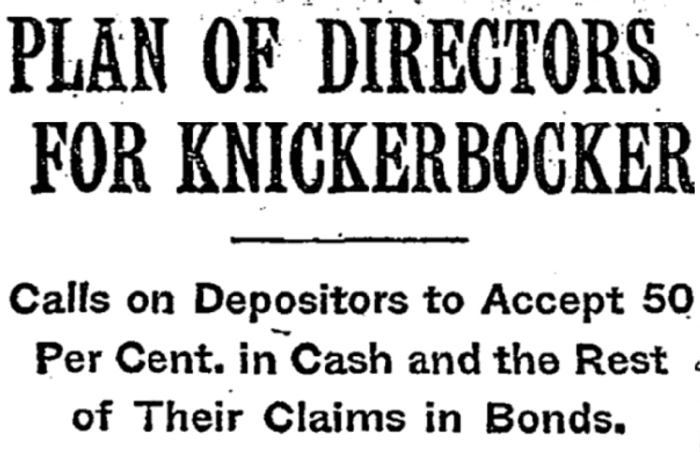

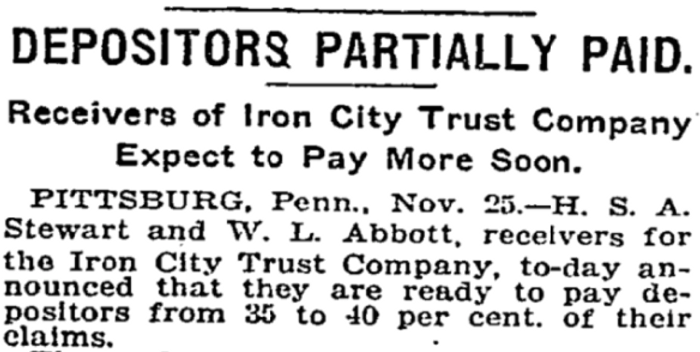

Now the real estate investments have soured. Households no longer want to renew their WMPs. This is what a shadow bank run looks like. Zhongzhi, parent company of the Zhongrong Trust, now has liabilities of 64 billion dollars to its assets of only 28 billion. That means investors would receive only 44 cents for each dollar of claims in a typical bankruptcy proceeding. That ratio is in the neighborhood of what was seen in the panic of 1907. On November 22nd, directors of the Knickerbocker Trust called on depositors to accept 50 cents per dollar of claims in cash, and the rest in IOUs. On November 25th, the receivers of Pittsburg’s Iron City Trust Company announced depositors would get only 35 to 40 cents per dollar of claims.

The New York Times. Nov 22, 1907

The New York Times. Nov. 25th, 1907

But the real estate sector started to crumble in 2021, why are the trusts faltering now? In a panic, it almost always comes back to the money market. You can’t pay investors 13 percent by investing their cash in bonds – like Evergrande’s – that pay only 8 percent. You have to use leverage, combining your own capital with borrowed money to increase returns, and that leverage comes from the money market. Over the last few centuries, the money market has taken different forms.

In 1907, America’s trust companies got leverage from the market for Call Money, short term loans of only a day or a few weeks. Their industrial stocks and bonds would be posted as collateral. Today, nearly all financial institutions depend, to some degree, on the market for Repurchase Agreements. “Repo” for short. These are also short term loans of only a day or a few weeks, with bonds most commonly posted as collateral. The repo market is the connection that Bloomberg, WSJ and the like have failed to make.

With a functioning repo market, even a Chinese trust with a crumbling real estate portfolio can live to meet its short term obligations; without one, they are toast. And China’s repo market is struggling. In mid-October, Reuters reported that China’s central bank lent $100 billion to the repo market because big borrowers were having trouble getting loans. That was the biggest so called “liquidity injection” since 2020.

On October 31st, the interest rate on repo loans blew out to 50 percent for some borrowers, and averages have been around 3.6. That doesn’t sound like a lot, but it’s double the central bank’s repo rate. So in the US, that would be like if financial institutions were having to borrow at 10.6 percent, double the Fed’s rate of 5.3. Hong Kong’s short term borrowing rate hit a 16-year high of 5.53 on November 26th.

In 1907 the trusts got hit from both ends – the rates on call money rose, threatening their ability to roll over debts and meet payment obligations. At the same time, the value of their investments fell. In 2023, China’s trusts are facing a similar dilemma. The decline in the property sector is tanking their investments – like those two cent Evergrande bonds – and with rocks in the engine of the repo market, they can’t even pay off investors with borrowed money.

There’s no way this continues without the effects being felt in the US and Europe. The only questions that remain are – to what extent, and when?